A customer applies for a home loan. Three weeks pass. They call the bank’s support line, wait forty minutes on hold, and are told the application is still under review. A small business owner receives a fraud alert at 2 AM, an unauthorized transaction has already cleared. By the time the bank opens, the money is gone. A new account applicant uploads their identity documents and waits five business days for KYC approval. A digital-first competitor approves the same documents in under a minute.

These are not hypothetical scenarios. They are happening today in the UAE, across India, throughout Southeast Asia and the Gulf and they represent exactly the kind of problems that Infin Mobile Solutions and AI in banking were built to solve.

We are a mobile-first technology company that designs and deploys AI-powered banking platforms built from scratch for the specific regulatory environments, customer expectations, and competitive pressures our clients face. In this article, we walk through the most critical challenges facing banks and financial institutions in 2026, and show you exactly how Infin Mobile Solutions address each one from AI fraud detection to digital mortgage platforms, from continuous KYC to agentic AI for financial crime prevention. Including our live deployment for Mashreq Bank in the UAE.

The State of AI in Banking in 2026: Past Experiment, Now Operational Imperative

A Market at $31 Billion and Accelerating

The global AI in banking market reached $31.29 billion in 2025 and is projected to hit $299 billion by 2033 a CAGR of 32.6%, according to Straits Research. Banking sector AI spending is forecast to exceed $53 billion in 2026, per Statista’s March 2026 analysis. McKinsey estimates generative AI could contribute $200–$340 billion in value annually to global banking. That is not a prediction about the future. It is the benchmark against which every bank’s digital strategy is now being measured.

Yet the gap between potential and reality is stark. According to AllAboutAI’s 2026 banking AI analysis, only 33% of banking organisations have begun scaling AI programs the remaining 67% are still stuck in experimentation or pilot phases. The window for strategic positioning is narrowing. The institutions that are deploying AI at scale now are not just reducing costs they are building a structural competitive advantage that becomes harder to close with every passing month.

The regulatory environment has also shifted. The EU AI Act, which came into force in February 2026, now applies directly to AI systems used in banking including credit scoring, KYC, and fraud detection models. And 75% of banks with over $100 billion in assets are currently implementing AI strategies, according to February 2026 industry data. The question is no longer whether to adopt AI it is whether your institution will be among the architects of this transformation or the institutions disrupted by it.

The AI Technologies Reshaping Banking Operations in 2026

AI in banking is not a single tool. It is a layered stack of capabilities that, when integrated into banking workflows, fundamentally changes what is operationally possible:

- Machine Learning and Predictive Analytics: Fraud detection, credit scoring, churn prediction, and customer lifetime value modelling with accuracy that rule-based systems cannot approach.

- Natural Language Processing (NLP): Conversational banking, automated customer query resolution, document data extraction, and compliance report generation.

- Computer Vision and OCR: Identity document reading and validation, forgery detection, and KYC automation processing documents that previously took days in under sixty seconds.

- Agentic AI: The defining shift of 2026. AI systems that do not just flag issues for human review but take autonomous action completing full KYC workflows, initiating fraud investigations from alert to case closure, and making credit decisions with minimal human intervention on routine cases.

- Generative AI: Customer communication drafting, loan officer summaries, compliance narratives, SAR reports, and personalised financial guidance at the scale of millions of customers simultaneously.

The Real Banking Problems in 2026 And How Infin Mobile Solutions Is Solving Them?

Every bank we work with faces a version of the same operational challenges. Here is what we hear most often in 2026 and how our solutions address each one directly.

Challenge 1: Fraud Has Become an AI Arms Race And Most Banks Are Losing

Banking fraud has reached unprecedented scale. Consumer fraud losses hit $12.5 billion in 2024, a 25% year-on-year increase, according to FTC data cited in Articsledge’s Complete 2026 Guide to AI Fraud Detection. Deloitte projects that generative AI-enabled fraud could reach $40 billion in the US alone in the coming years. And a 2026 industry poll cited by The Paypers confirmed that AI is now seen as the single most impactful external factor shaping the financial crime landscape, cited by 37% of financial crime professionals — ahead of increasingly sophisticated criminality and regulatory change.

The nature of the threat has evolved. In 2026, fraudsters are not just individuals — they are operating as AI-augmented crime rings. As Experian’s 2026 fraud predictions document, fraudsters now deploy agentic AI to run thousands of adaptive, real-time conversations in parallel, personalised to each victim making romance scams, investment fraud, and authorised push payment fraud industrial in scale. AI agents handle the early trust-building phase of a scam; human fraudsters step in only when the target is ready to transfer money. Traditional rule-based detection systems cannot see this pattern.

Infin Mobile Solutions builds AI fraud detection systems that counter this threat with equal sophistication. Our machine learning models monitor every transaction, login, and account interaction in real time analyzing behavioural signals, device fingerprints, geographic consistency, transaction timing, and cross-account network patterns simultaneously. When the system detects an anomaly consistent with a fraud pattern whether known or novel it acts immediately. The transaction is flagged or blocked. The customer receives an instant push notification. The bank’s risk team receives a prioritized alert. The system does not wait for business hours, and neither do today’s fraudsters.

In 2026, we also integrate agentic AI into fraud response workflows. Rather than simply flagging suspicious transactions for human review, our agentic systems can initiate verification workflows, request supporting documentation from the customer, and escalate to human investigators only when genuine complexity warrants it. This is consistent with the direction described in Emburse’s 2026 AI Fraud Detection Guide: agentic AI functioning as a continuous compliance auditor, not just a detection layer.

- Real-time behavioral monitoring across all channels mobile, web, ATM, SWIFT, and in-branch

- Graph Neural Networks (GNNs) for detecting coordinated fraud networks across accounts

- Instant multi-channel alerts: push notification, SMS, and in-app no delay, no business hours

- Agentic fraud response: AI initiates verification workflows autonomously, escalating only genuine complexity

- Continuous model learning: the system improves with every fraud attempt it encounters

- EU AI Act and FATF AMLD6 compliant architecture: full explainability and audit trail for every AI decision

Challenge 2: Traditional KYC Is Broken Synthetic Identity Fraud Has Collapsed the Old Model

One-time KYC at account opening is no longer a viable security model. US lenders faced $3.3 billion in exposure to suspected synthetic identities in the first half of 2025 alone, according to TransUnion data reported by BankInfoSecurity in January 2026. The barrier to creating fake identities that pass verification has collapsed. As one fraud investigator documented, building a fully functioning synthetic identity capable of passing basic verification checks took approximately seven minutes using publicly available AI tools.

What makes synthetic identity fraud particularly damaging is its patience. Fabricated identities blend into legitimate customer traffic, remain dormant for months, and are activated for fraud long after the initial KYC check is complete. Experian’s 2026 predictions describe the necessary response: continuous KYC, where customer risk profiles are updated in real time throughout the customer lifecycle not just at onboarding. Banks replacing static KYC with ongoing, risk-based identity monitoring is now the industry direction confirmed by regulators and practitioners alike.

Infin Mobile Solutions builds digital KYC and continuous identity verification platforms that address both sides of this challenge. At onboarding, our OCR systems extract data from identity documents instantly passports, Emirates ID, Aadhaar, and 12,000+ government-issued ID formats globally. Computer vision validates document authenticity and flags the AI-generated forgeries that now account for a growing share of KYC fraud. Facial recognition with liveness detection confirms physical presence and blocks deepfakes. The entire onboarding process completes in minutes. And beyond onboarding, our continuous monitoring layer maintains a live risk profile for every customer updating it with every transaction, login, and behavioral signal, so that a synthetic identity that slips through initial checks cannot operate undetected indefinitely.

- OCR document extraction: reads and validates IDs, passports, utility bills, bank statements instantly

- AI document authentication: detects AI-generated forgeries, tampered documents, and reused identity images

- Biometric facial recognition with liveness detection: blocks deepfakes and photo-of-photo attacks

- Continuous KYC: ongoing risk profile monitoring throughout the customer lifecycle, not just at onboarding

- Automated AML: real-time sanctions screening, PEP checks, and adverse media monitoring

- Compliance-ready audit trail: every KYC decision logged, explained, and exportable for regulatory review

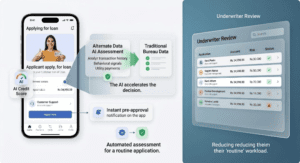

Challenge 3: Loan Processing Takes Too Long and Hands Business to Faster Competitors

AI-powered loan underwriting is already delivering measurable results. Major US banks reported 13% average operational cost reduction in 2025, with AI-driven loan processing 25% faster than manual underwriting, according to AllAboutAI’s 2026 banking AI analysis. Meanwhile, AI-driven credit scoring can increase loan approval rates by 15% without increasing risk, according to verified industry data. Yet the majority of banks in our markets the UAE, India, Saudi Arabia, and Southeast Asia are still running manual or semi-manual origination processes that take days where competitors take hours.

Every day a loan application sits in a queue is a day a digital-first lender can win that customer. Infin Mobile Solutions builds AI loan origination platforms that compress the time between application and decision to hours or minutes for straightforward applications. Our AI credit scoring models assess traditional bureau data alongside alternative signals: transaction history, account behaviour, payment patterns, and in-market indicators specific to each loan product. Provisional approvals are issued automatically for applications that meet risk criteria. Complex cases are routed to underwriters with an AI-generated risk summary so the human decision takes minutes, not hours. Everything document submission, verification, e-signature, and disbursal happens within the mobile app.

- AI credit scoring using traditional bureau data and alternative behavioral signals

- Instant provisional approval for qualifying applications decision in minutes

- Digital document submission and automated verification: income statements, employment records, tax returns

- Borrower dashboard: real-time application status, outstanding balance, repayment schedule, due reminders

- Digital disbursal: loan credited automatically upon e-signature completion

- Loan restructuring, pre-payment, and top-up requests handled entirely in-app

Challenge 4: Customer Service Is Still Expensive, Slow, and Unavailable When Customers Need It Most

Conversational AI in banking has moved past proof-of-concept. Bank of America’s virtual assistant Erica has crossed 3 billion client interactions, supporting nearly 50 million users with approximately 58 million monthly interactions, according to AllAboutAI’s banking AI data. And according to KMS Technology’s 2026 banking AI trends analysis, AI is expected to raise front-office banking productivity by 27–35% by 2026. The economics of AI-powered customer service are no longer theoretical they are being reported in earnings calls.

A customer with a question about their statement at 11 PM on a Sunday should not have to wait until Monday morning. A business owner trying to understand a foreign exchange rate should not need to navigate a phone tree. A retail customer disputing a transaction should not be required to visit a branch. Infin Mobile Solutions builds AI-powered conversational banking platforms chatbots and virtual assistants integrated into mobile apps and websites that handle the majority of routine banking interactions automatically, 24 hours a day, in multiple languages. When a query exceeds the AI’s capability, the system escalates to a live agent with the full conversation context already transferred so the customer never has to repeat themselves.

- 24/7 AI virtual assistant: balance inquiries, transaction disputes, card management, loan status, and more

- NLP-powered: understands natural conversational language not just menu-driven keyword triggers

- Multilingual: English, Arabic, Hindi, Urdu, and other languages based on customer preference

- Seamless human escalation: full context transferred, no repetition for the customer

- Proactive notifications: AI sends payment reminders, fraud alerts, and personalised product nudges automatically

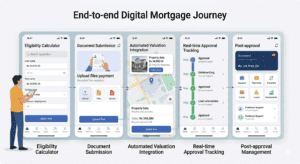

Challenge 5: Digital Mortgage Is Still Anchored to Paper and Branch Visits

Applying for a property mortgage at most banks in the UAE, India, and across the Gulf still involves physical document submission, multiple branch visits, and approval timelines that stretch to weeks. This is a losing proposition against digital-first lenders who have rebuilt the mortgage experience from the customer’s perspective starting with the assumption that every step should happen on a phone.

Banks lose mortgage business not just to lenders with lower rates they lose it to lenders with a faster, more transparent process. A customer who receives a provisional approval in 24 hours from a mobile platform is not returning to a bank that requires three weeks and three in-person visits. Infin Mobile Solutions builds end-to-end digital mortgage platforms that bring the full property finance lifecycle eligibility checking, document submission, credit assessment, real-time status tracking, and ongoing account management into a single mobile interface. AI handles the routine verification steps that previously required manual processing at every stage.

- AI eligibility calculator: instant provisional borrowing capacity based on income, credit, and property data

- Digital document submission: income statements, employment contracts, property documents all in-app

- Integration with property valuation services and credit bureaus: automated assessment, no manual handoffs

- Real-time application tracking: customer sees exactly where their application stands at every step

- Post-approval mortgage dashboard: payments, amortization schedule, statements, and support in one place

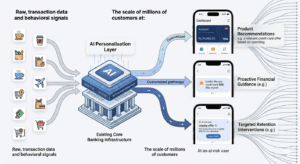

Challenge 6: Banks Have the Data to Personalise at Scale But Most Are Not Using It

Banks implementing AI-driven personalisation report a 25–35% increase in product adoption, 40% improvement in customer satisfaction, and 15–20% growth in revenue per customer, according to KMS Technology’s 2026 AI trends analysis. AI-driven personalisation also delivers 5x more clicks on targeted offers versus generic communications. The data needed to achieve this already exists inside every bank’s transaction systems. Most banks are not using it at scale because they have not built the AI layer that makes it actionable.

Infin Mobile Solutions builds AI personalisation platforms that sit on top of existing core banking systems, analysing each customer’s transaction behaviour, product usage, life-stage signals, and engagement patterns to deliver the right recommendation at the right moment. A customer consistently saving over six months sees a fixed deposit offer. A business account holder with growing monthly transaction volumes sees a working capital facility. A customer who just sent an international transfer sees a competitive FX rate product. This is not mass marketing with segments it is one-to-one guidance delivered to a million customers simultaneously.

- Behavioural analytics: AI reads transaction patterns to understand each customer’s current financial position

- Real-time product recommendations: right offer, right moment, right channel in-app, push, or email

- Customer lifetime value modelling: identifies high-value customers for priority service and retention

- Churn prediction: flags customers at risk of leaving and triggers proactive retention interventions

- AI wealth management nudges: savings goals, investment prompts, spending insights automatically delivered

Our AI Banking Solutions: What Infin Mobile Solutions Builds?

Every Infin Mobile Solutions banking platform is engineered around a specific operational or customer problem. We do not sell product templates. We build custom platforms for the market, regulatory environment, and technical infrastructure of each client.

Digital Banking Mobile Applications

Full-featured retail and business banking apps iOS and Android that bring every banking service into a single, intuitive mobile interface. Account management, payments, transfers, cards, loans, investments, and customer support all with AI personalization and fraud detection built into every interaction layer

.

AI Fraud Detection and Security Systems

Real-time, multi-channel fraud monitoring using machine learning models trained on behavioural and transactional signals. In 2026, our systems incorporate agentic AI that moves beyond flagging taking autonomous action to initiate verification, lock compromised accounts, and generate compliance documentation, with human oversight at the decision points that require it.

Continuous Digital KYC and Account Onboarding

Digital onboarding platforms that take new customers from document submission to account activation in minutes with OCR, computer vision, liveness detection, and automated AML screening working in concert. Beyond onboarding, our continuous KYC layer maintains a live risk profile for every customer throughout their lifecycle.

AI Loan Origination and Credit Management

Loan platforms using AI credit scoring to accelerate decisions, expand credit access to customers underserved by traditional bureau-based models, and reduce underwriter workload through automated assessment of routine applications. From application to disbursal entirely in the mobile app.

Digital Mortgage Platforms

End-to-end digital mortgage solutions that bring the full property finance lifecycle into a mobile interface eligibility calculators, document submission, automated valuation integration, real-time approval tracking, and post-approval management.

Conversational Banking and AI Customer Service

AI chatbot and virtual assistant integrations handling routine banking queries 24/7 in multiple languages with seamless escalation to human agents for complex cases. Customers get instant answers. Banks reduce support costs and improve satisfaction scores simultaneously.

Personalisation and Analytics Platforms

AI personalisation layers built on top of existing core banking infrastructure using transaction data and behavioural signals to deliver relevant product recommendations, proactive financial guidance, and targeted retention interventions at the scale of millions of customers.

Live Deployment: Mashreq Bank Digital Mortgage Platform, UAE

The clearest way to understand what Infin Mobile Solutions builds is to look at what we have delivered in production. Our digital mortgage platform for Mashreq Bank one of the UAE’s leading and most digitally progressive financial institutions is a live deployment that demonstrates AI-powered banking transformation at enterprise scale in a regulated market.

Client: Mashreq Bank, UAE | Project: Digital Mortgage Platform | Tech: React.JS · Node.JS | Market: UAE | InfinMobile.com/client/mashreq-bank-app

The Problem Mashreq Came to Us With

Mashreq Bank is one of the UAE’s most established financial institutions, consistently ranked among the most digitally ambitious banks in the Gulf. Yet their mortgage origination process like that of most traditional banks involved physical document submissions, multiple touchpoints requiring branch attendance, and processing timelines that could not compete with the speed customers now expect from the digital-first lenders entering the UAE market.

The brief was clear: build a digital mortgage platform that brings the entire property finance journey into a seamless digital experience. One that eliminates unnecessary branch visits, reduces processing time through intelligent automation, integrates with existing systems without requiring a full infrastructure overhaul, and gives customers real-time visibility throughout a process that had previously felt opaque.

What Infin Mobile Solutions Built?

Infin Mobile Solutions designed and developed a comprehensive digital mortgage platform on React.JS and Node.JS selected for performance, flexibility, and clean integration with Mashreq’s existing core banking infrastructure.

The platform gave customers an AI-powered eligibility calculator that provided instant provisional borrowing capacity based on income data, employment status, and property details so applicants understood their position before completing a full application. The document submission module allowed customers to upload all required materials income statements, employment contracts, property documents through the platform, with automated validation at each step. Automated integration with credit bureau APIs and property valuation services eliminated the manual handoffs that had previously extended processing timelines. A real-time status tracking dashboard gave applicants complete visibility into exactly where their application stood at every stage. And post-approval, a dedicated mortgage management interface allowed customers to view their amortization schedule, make payments, access statements, and contact their relationship manager all without visiting a branch.

Technology Stack

- Frontend: React.JS

- Backend / APIs: Node.JS

- Integrations: Credit bureau APIs, property valuation services, core banking middleware

- Deployment: Cloud-hosted with UAE regulatory compliance and enterprise security architecture

The Outcome

The platform transformed Mashreq’s mortgage origination from a largely physical, document-heavy process into a streamlined digital journey that customers could complete from their phone. Automating the document verification and credit assessment steps that had previously required manual intervention at multiple points reduced processing time significantly. And customers gained transparency into a process that had previously felt unpredictable a meaningful shift in experience for the most significant financial decision most customers will make.

It demonstrates the principle that sits at the core of everything Infin Mobile Solutions builds: the best banking technology does not simply digitise existing processes. It reimagines them from the customer’s perspective and then builds the infrastructure to deliver that reimagined experience at scale, within the regulatory constraints that banking demands.

View the full Mashreq Bank case study: InfinMobile.com/client/mashreq-bank-app

Why Mobile-First Banking Technology Is Non-Negotiable in 2026?

In the UAE, mobile internet penetration exceeds 99%. India has over 750 million smartphone users. Across the Gulf and Southeast Asia, the majority of banking interactions balance checks, transfers, loan applications, investment decisions are now initiated on mobile devices. Banking technology that is not genuinely built mobile-first is not built for the markets that matter.

Mobile-first also changes what AI can deliver. A mobile banking platform with AI embedded is not just a convenient interface it is a continuous data stream that feeds fraud detection models, personalisation engines, and behavioural analytics systems with real-time signals from millions of interactions. The more customers engage, the smarter the AI becomes. The smarter the AI becomes, the better the experience and the lower the fraud and operational cost. This virtuous cycle is what Infin Mobile Solutions engineers into every platform.

In 2026, mobile-first banking is also a competitive survival requirement. Digital-native neobanks and fintech challengers have been mobile-first from their first line of code. Traditional banks that treat mobile as a supplement to branch banking rather than the primary channel are ceding ground to competitors who have already built the infrastructure customers now expect as standard.

How Infin Mobile Solutions Builds Banking Solutions?

We Start With Regulation, Not Just Technology

Banking is one of the most heavily regulated industries in the world and in 2026, the regulatory environment is more demanding than ever. The EU AI Act now requires explainability and audit trails for AI systems used in credit scoring and KYC. UAE Central Bank guidelines govern data residency and customer authentication. RBI regulations in India set standards for digital lending. SAMA rules apply in Saudi Arabia. Every Infin Mobile Solutions banking platform is designed with the applicable regulatory framework as a foundational architecture requirement not a compliance checkbox at the end. The Mashreq platform was built with UAE regulatory requirements embedded from the first design decision.

Security Is the Foundation, Not an Addition

Banking data is the most sensitive category of personal and financial information that exists. We build with security-first architecture: end-to-end encryption for all data in transit and at rest, multi-factor and biometric authentication, role-based access controls, full audit logging, and deployment on enterprise-grade cloud infrastructure certified for banking data in our target markets. In 2026, this also means building AI systems that are explainable because regulators, including under the EU AI Act, now require that AI decisions affecting customers can be understood and audited.

Integration, Not Replacement

Most banks cannot and should not replace their core banking systems. Infin Mobile Solutions builds platforms that integrate with existing infrastructure using APIs, HL7 FHIR-equivalent financial standards, and open banking protocols rather than requiring a full technology overhaul. The Mashreq mortgage platform integrated cleanly with existing systems through Node.JS APIs and credit bureau connections. Faster deployment, lower total cost, no disruption to the banking operations customers depend on.

Where AI in Banking Is Heading And Where Infin Mobile Solutions Is Already Building?

The defining shift of 2026 is the transition from AI that assists humans to AI that acts. Agentic AI systems that complete workflows autonomously rather than simply flagging issues for human review is moving from pilot to production across leading financial institutions.

In KYC and AML, agentic AI systems are now completing the full onboarding and compliance workflow including document verification, sanctions screening, PEP checks, and adverse media monitoring without human intervention on routine cases, with escalation only for genuine complexity. McKinsey’s analysis of this transition documents 15–20% productivity uplifts in early deployments. At Infin Mobile Solutions, we are integrating agentic capabilities across our fraud, KYC, and loan origination platforms not as a future roadmap item, but as a present deployment architecture for clients who are ready to move past pilot.

Beyond agentic AI, the developments we are building toward in 2026 and beyond include:

- Continuous KYC at scale: live risk profiling of every customer throughout their lifecycle — replacing the static checkpoint model that synthetic identity fraud has already broken.

- Government digital identity integration: as UAE(Emirates ID), India (Aadhaar), and other markets deploy national digital ID frameworks, our platforms will integrate directly accelerating onboarding, reducing fraud, and eliminating the document submission friction that remains one of the biggest drop-off points in customer acquisition.

- Federated learning for fraud intelligence: AI models trained collaboratively across institutions without sharing raw customer data enabling collective fraud intelligence while preserving privacy and regulatory compliance.

- Predictive credit intelligence using alternative data: assessing creditworthiness from utility payments, mobile transaction patterns, and rental history expanding credit access to the large portion of Gulf and South Asian populations without traditional bureau files.

- Voice and multimodal banking: AI systems that handle banking through voice commands and image uploads not just text inputs, significantly expanding accessibility for customers who prefer conversational interaction.

The Problems Are Immediate. The Solutions Are Ready. The Gap Is Closing For Your Competitors If Not for You.

Fraud that arrives faster than your detection systems. KYC onboarding that is simultaneously losing good customers and letting fraudulent ones through. Loan processing that takes weeks while digital-first competitors approve in hours. Customer service that is only available during business hours. Mortgage applications that require a branch visit in 2026. These are not distant threats. They are the operational realities that banks across the UAE, India, the Gulf, and Southeast Asia are navigating right now.

Infin Mobile Solutions builds the mobile-first, AI-powered platforms that solve these problems built for the regulatory environments, customer expectations, and competitive pressures of the markets we serve. Our work with Mashreq Bank demonstrates this approach at enterprise scale in the UAE. It is one example of what is possible when technology is built around the actual operational and customer problems a bank faces rather than adapted from a generic product catalogue built for a different market.

If your institution is facing any of these challenges or if you are ready to build a banking platform that gives you a structural advantage in the markets you serve we would like to hear from you.

Explore our full banking and fintech portfolio at infinmobile.com, or contact our team today to begin a discovery conversation.

Frequently Asked Questions:

What specific banking problems does Infin Mobile Solutions solve with AI in 2026?

Infin Mobile Solutions builds AI-powered mobile banking solutions that address the critical operational and customer challenges banks face today: real-time AI fraud detection including against agentic fraud attacks, continuous digital KYC to counter synthetic identity fraud, AI-accelerated loan origination, digital mortgage platforms, conversational AI customer service, and AI personalisation for product recommendations and customer retention. Every solution is built around a specific problem not as a generic product.

How does AI fraud detection work in a banking mobile app in 2026?

Infin Mobile Solutions’s 2026 AI fraud detection systems go beyond flagging transactions for review. Our machine learning models monitor every interaction in real time using behavioural signals, device fingerprints, and cross-account network analysis. When an anomaly is detected, agentic AI can initiate verification workflows, lock compromised accounts, and escalate to human investigators autonomously, 24 hours a day. The system is built with EU AI Act explainability requirements, maintaining a full audit trail for every AI decision.

What is continuous KYC and why does Infin Mobile Solutions use it instead of one-time onboarding?

One-time KYC at account opening is no longer a sufficient fraud defence. US lenders faced $3.3 billion in exposure to synthetic identities in just the first half of 2025. Synthetic identities can pass initial document checks and remain dormant in banking systems for months before being activated for fraud. Infin Mobile Solutions’s continuous KYC platforms maintain a live risk profile for every customer updated with every transaction, login, and behavioural signal so fraudulent accounts cannot operate undetected after they pass onboarding.

What was the Mashreq Bank digital mortgage platform Infin Mobile Solutions built?

Infin Mobile Solutions built a comprehensive digital mortgage platform for Mashreq Bank, one of the UAE’s leading financial institutions. Built on React.JS and Node.JS, the platform enabled customers to check mortgage eligibility, upload documents, track application status in real time, and manage their mortgage post-approval all through a digital interface, without requiring branch visits. It integrated with Mashreq’s existing core banking systems, credit bureaus, and property valuation services through clean API connections.

Which markets does Infin Mobile Solutions serve for AI banking solutions?

Infin Mobile Solutions builds AI banking platforms for clients across the UAE, India, Southeast Asia (Singapore, Malaysia), South Africa, Saudi Arabia, and other Gulf and emerging markets. Our solutions are specifically engineered for the mobile-first infrastructure, regulatory frameworks including UAE Central Bank, RBI, SAMA, and the EU AI Act where applicable and multilingual customer populations of these regions.

Is Infin Mobile Solutions’s banking software compliant with the EU AI Act and banking regulations?

Yes. Every Infin Mobile Solutions banking platform is built with the applicable regulatory framework as a foundational architecture requirement. In 2026, this includes the EU AI Act for AI systems used in credit scoring, KYC, and fraud detection requiring explain ability, audit trails, and human oversight mechanisms at defined decision points. It also includes UAE Central Bank guidelines, RBI requirements, SAMA regulations, GDPR, AML/KYC standards, and PCI DSS for payment data.

- Tags:

- Agentic AI

- AI Banking 2026

- AI Customer Service

- AI Fraud Prevention

- AI in Banking

- Banking Automation

- Banking Innovation

- Banking Personalization

- Banking Technology

- Digital Banking

- Digital KYC

- Digital Mortgage Platform

- Financial Technology

- Fintech Solutions

- Fintech Trends 2026

- Fraud Detection AI

- Generative AI in Banking

- Mobile Banking

- Neobank Technology

- Predictive Analytics Banking